Findings

Table of Content

Overview

Demographics

Discussion of Findings

Codebook

Financial Constraints

Financial Strategies and Importance of Support System

Structural Issues and Expectations for the Government

Perspectives on the Child Tax Credit

Overview

Our research team undertook a series of structured interviews at Trinfo Cafe’s VITA site, engaging Hartford residents with and without children under 18. The primary objective was to delve into their financial circumstances and gauge their perspectives on the proposed child tax credit. We conducted a total of 22 interviews, averaging 15 minutes each. Questions centered on tax refunds, overall financial status, and opinions regarding a potential Connecticut Child Tax Credit. Additionally, participants were invited to share their perspectives on the proposed credit via video, with assurance of complete control over their contributions.

Demographics

Race and Gender: The demographic landscape reflected a vast diversity of identities, with 50% identifying as Black, 40% as Hispanic, and a majority, constituting 75%, identifying as female, while the remaining 25% identified as male.

Long-Term Hartford Residents: Notably, 45% of the residents have established roots in Hartford for over two decades.

Age: In our study comprising 22 interviewees, we encountered a diverse range of individuals, spanning ages from 25 to 79, with an average age of 46.

Household Size: These participants hailed from varied family structures and household compositions, with household sizes fluctuating between single-person households and those accommodating up to six individuals, averaging two people per household.

Discussion of Findings

Codebook

| Theme | Code | Code Definitions |

| Financial Constraints | ||

| Income/Average Income | Average: Refers to the total income earned by our participants divided by the total number 22. | |

| Struggle to Pay Basic Necessities | Situations where households do not generate enough financial resources on a monthly basis to meet their basic needs and expenses (such as housing, food, utilities, and other essential requirements). | |

| Unexpected Expenses | Not being able to cover emergency and unexpected expenses such as an illness, a major repair, etc. | |

| Cycle of Debts | A recurring pattern where individuals or households continuously accumulate debt without being able to fully repay it, leading to a persistent state of indebtedness. This cycle often involves borrowing money to cover expenses, then struggling to make payments due to high interest rates or other financial obligations, which in turn necessitates further borrowing, perpetuating the cycle. | |

| Inflation/Cost of Living | Individuals mention changes in the cost of living which are often influenced by factors such as inflation, wage levels, housing market conditions, and government policies. | |

| Child Development Pace | The challenge of keeping up with expenses due to fast growth. | |

| Financial Strategies and Importance of Support System | ||

| Selling goods | The practice of generating funds or raising capital by selling their assets. | |

| Relying on other extended family members or community. | Depending on relatives outside of their immediate family for financial support or assistance. This strategy may include borrowing money, or pooling resources with extended family members or their community to meet financial needs. | |

| Budgeting Strategies/Prioritizing | Allocating limited financial resources to address the most critical needs or goals first. | |

| Resorting to Credit Cards | Using credit-card borrowing as a means to meet immediate financial needs or cover expenses when other funds are not readily available. | |

| Looking Forward to Tax Time | Anticipating and relying on tax refunds or credits as a means to improve one’s financial situation or address specific financial needs. | |

| Structural Issues/Expectations From Government | ||

| Economic Opportunities | Being able to use the CTC on future savings, specifically for emergencies. | |

| Infrastructure/Transportation | The need for own transportations (car) and its impact on individual’s economy. | |

| Childcare | Using the CTC to increase children’s quality of life by making childcare and education services more available. | |

| A conflict in personal finance. Having to prioritize basic needs over other wants that would increase the quality of life. | ||

| Lack of Financial Mobility | The feeling of a cycle of poverty being prolonged, or the lack of opportunities to advance economically. | |

| Feelings of unappreciation | The emotional burden of not having one’s work and effort recognized because of the public perception that ‘it is not enough.’ | |

| Losing Faith in G | The low or inexistent expectation for public institutions and the government on providing support and solutions to those in need. | |

| Perspectives on CTC | ||

| Support | Being in favor of the implementation of a CTC, whether it is $200 or $600. | |

| ‘Anything Helps’ | The perception is that no matter the amount given as a CTC, it will be valuable for its recipients. | |

Financial Constraints

The gross income of participants ranged from $8,600 – $46,500 with an average of $26,885/year. This is well below the ALICE threshold, a threshold that our community partner uses as the minimum annual income one can “comfortably” survive off of.

Financial constraints can manifest in various forms, significantly impacting individuals and households. 40% of interviewees mentioned that they do not make enough to cover monthly expenses. A common struggle emerges when households find it challenging to cover necessities every month, including housing, food, utilities, and other essential expenses. For instance, 54% of participants mentioned that they struggle to pay rent.

Moreover, unforeseen financial burdens, such as sudden illnesses or major repairs, can exacerbate these challenges by creating unexpected expenses that strain already limited resources. 53% of participants stated that they would not be able to cover an unexpected expense of $400.

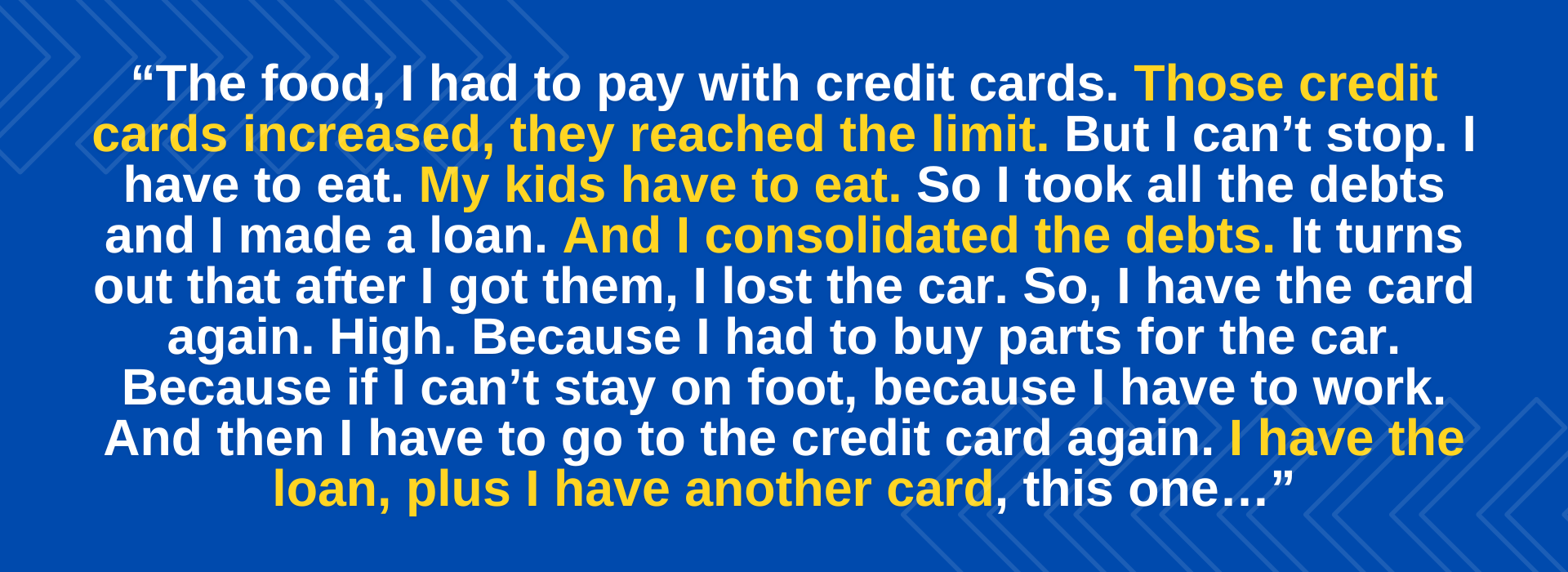

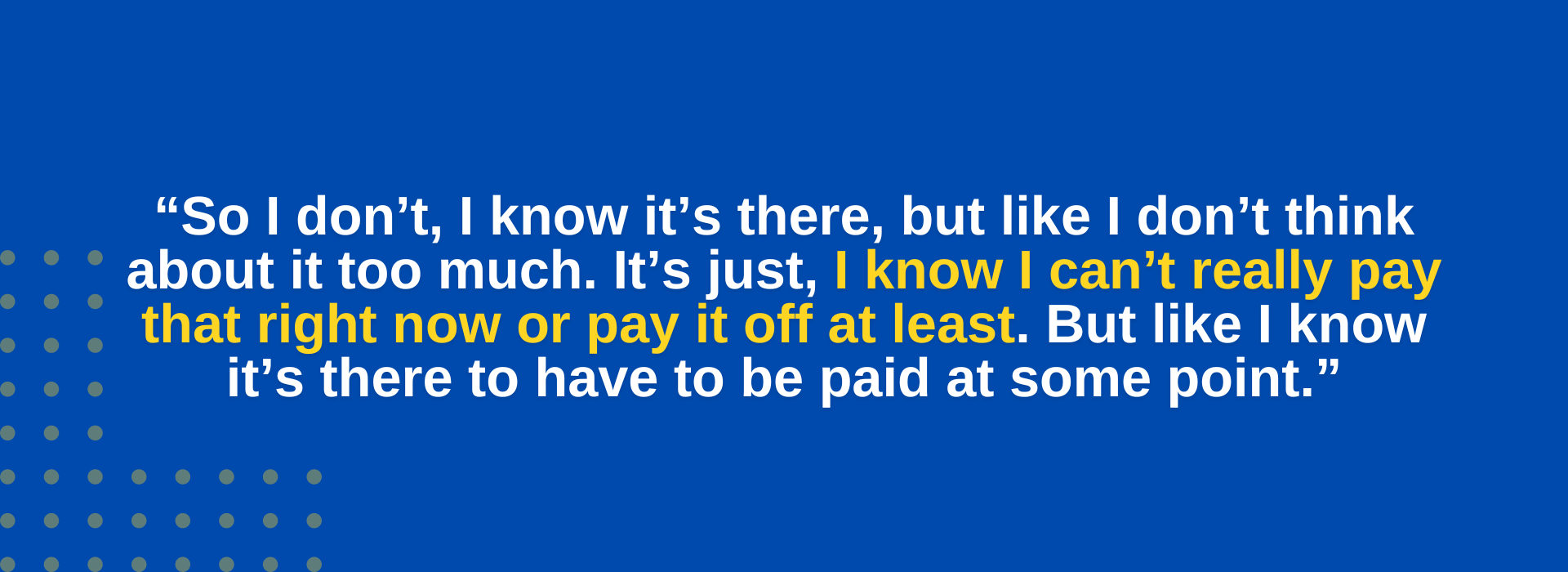

Additionally, a cycle of debts often ensues, wherein individuals or households continuously accumulate debt without the means to fully repay it, perpetuating a state of indebtedness. This cycle typically involves borrowing to cover expenses, struggling with high interest rates or other financial obligations, and resorting to further borrowing to meet ongoing needs. 59% of participants interviewed mentioned that they struggle with debts.

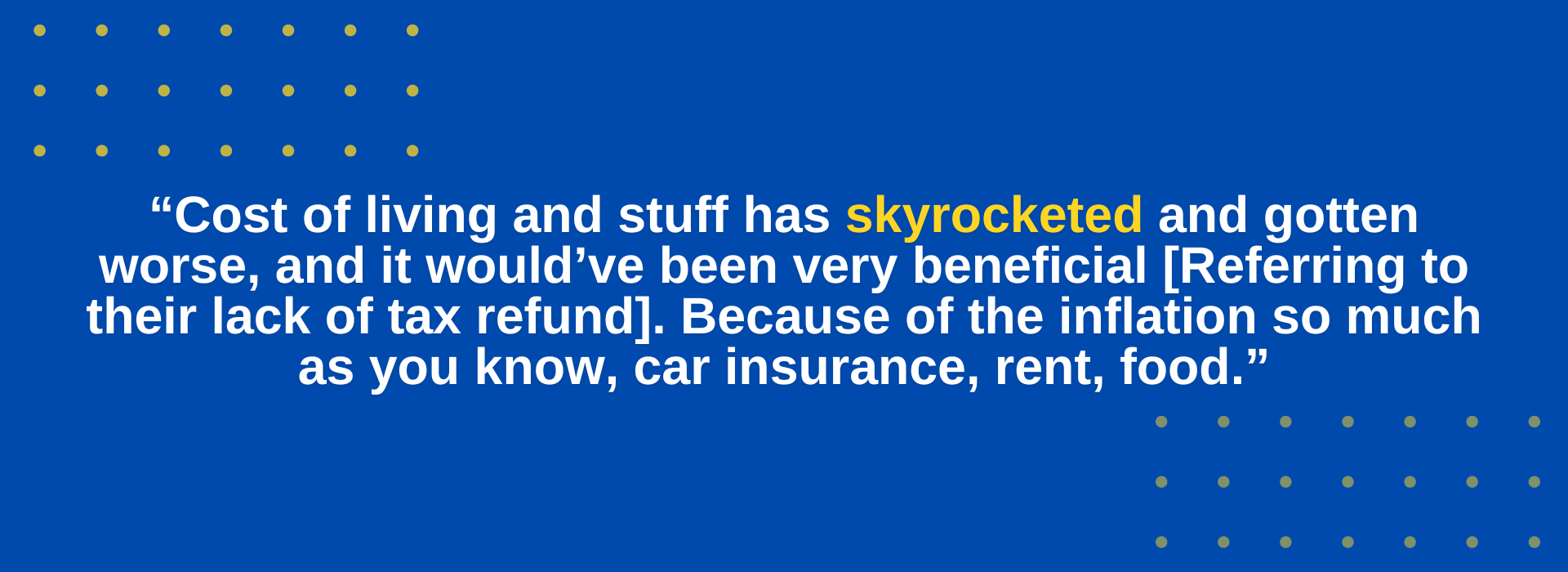

Furthermore, the impact of inflation and the rising cost of living exacerbates financial strain, as individuals contend with changes influenced by factors like inflation rates, wage levels, housing market conditions. The issue of inflation and the cost of living was mentioned by 11 of our 22 interviewees.

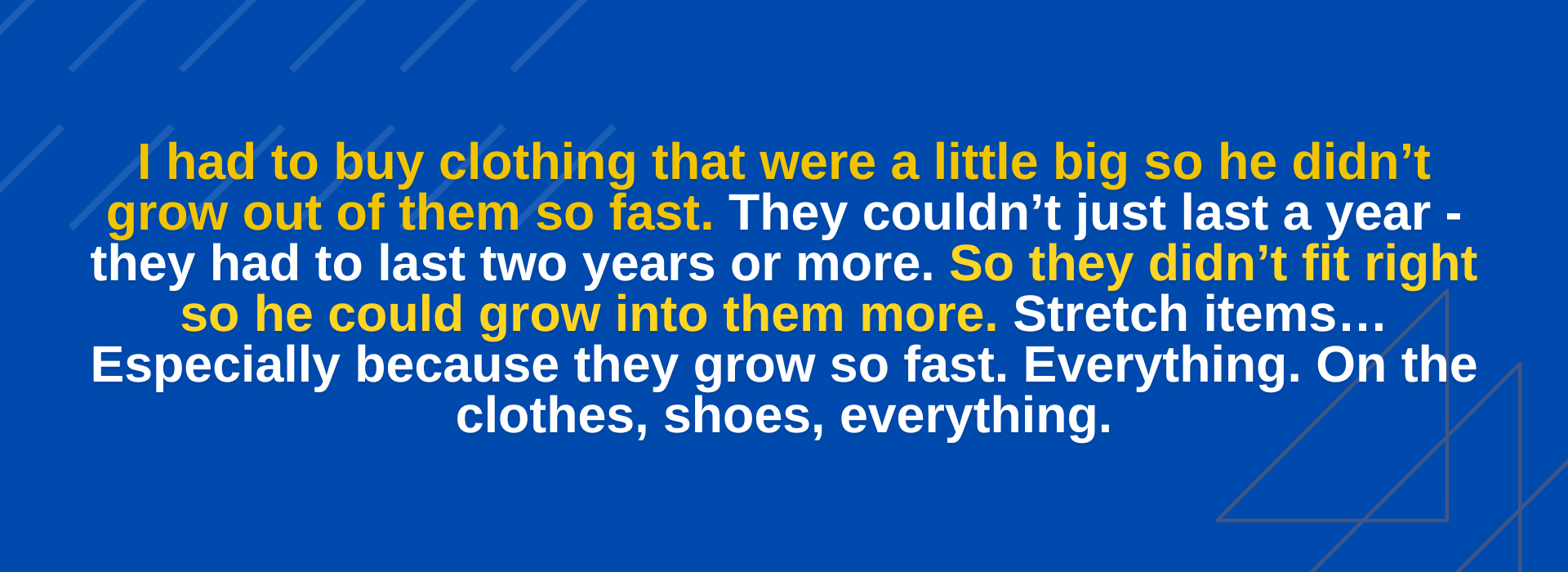

Finally, individuals mentioned the expenses of raising children as another layer of financial pressure, as families navigate the challenge of keeping up with the expenses associated with raising children. Concerns about the pace of child development were mentioned by 4 of our participants throughout our interviews.

Financial Strategies and the Importance of Having a Support System

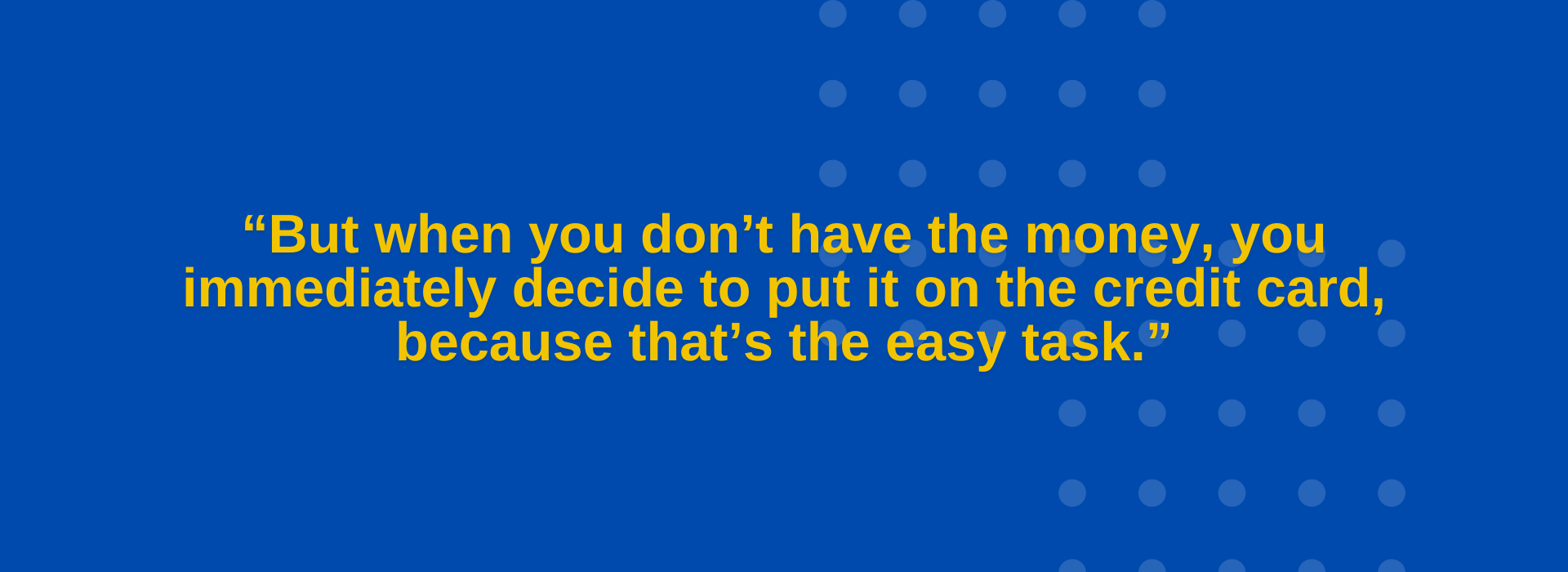

The findings from our interviews shed light on the pervasive challenges individuals face in managing their finances, often resorting to credit cards to cover basic expenses after prioritizing bills like rent and utilities.

This reliance on credit perpetuates a cycle of debt familiar to many American families, wherein the inability to cover essential costs leads to accumulating debt that becomes increasingly difficult to pay off.

![“[I] had to make a 10, 000 loan to be able to pay for the cards because I repeat, when I was short, my husband had lost his job in 2023. I had to resort to what I was charging to be able to pay for the house and to be able to pay some debts.”](https://action-lab.org/family-finance/files/2024/04/Findings-Sixth-Quote.png)

Tax time emerges as a critical juncture for many, offering a brief respite as they utilize refunds to alleviate credit card burdens.

Furthermore, our research underscores the significance of support systems, with respondents acknowledging the necessity of turning to extended family members or their community for financial assistance.

This reliance on external networks highlights the interconnectedness of individuals in navigating financial challenges, often through strategies such as borrowing money or pooling resources. In essence, these findings underscore the importance of effective budgeting strategies and the role of support systems in alleviating financial burdens and fostering financial stability.

Structural Issues/ Expectations for the Government

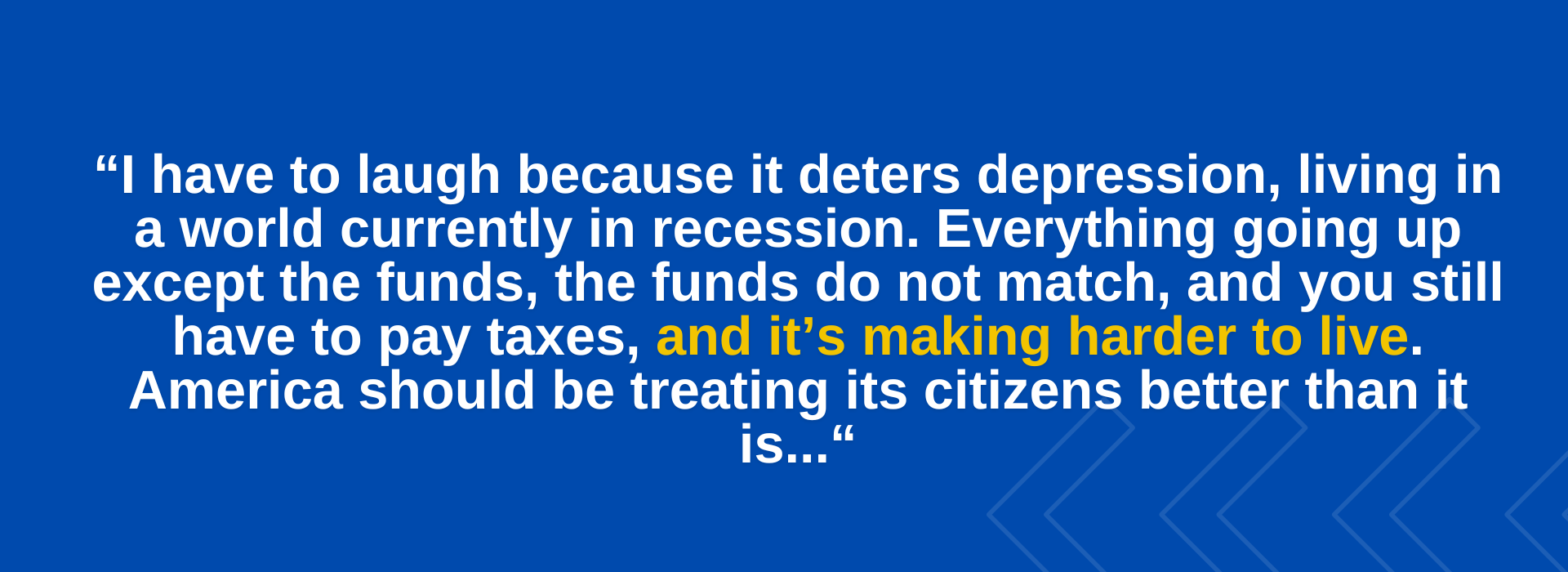

Through our research on the importance of the child tax credit, several significant structural issues have emerged. While analyzing demographic and financial data revealed crucial insights, we noticed patterns in many people’s perspectives in regard to structural issues and expectations from the government. A prevailing sentiment was that the people of Connecticut are losing faith in their government, as they continue to have trouble meeting basic needs their belief in the system has gone down. This shift in attitude points to structural problems in the state of Connecticut.

In the 22 interviews conducted, the question of dignity vs survival came up 22 times. So not only are Connecticut families struggling to survive, but they also feel ashamed about their struggles; a reality our literature review has deemed highly avoidable.

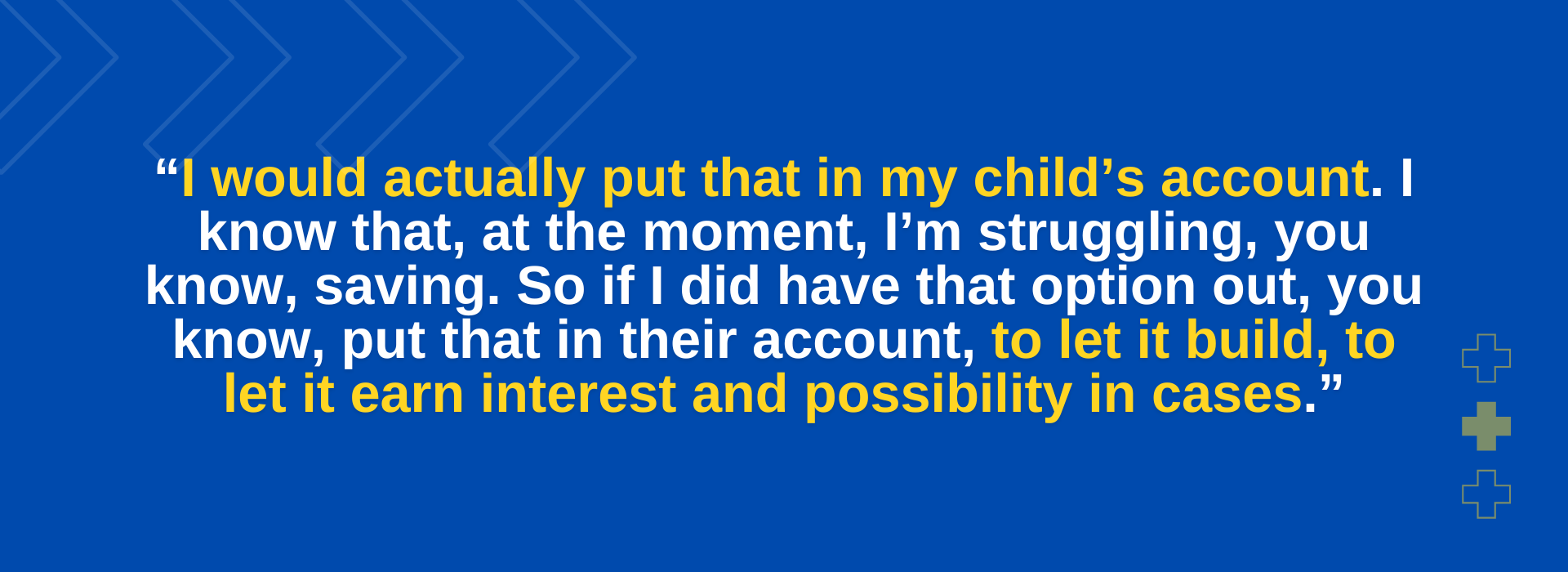

A Tax Credit helps preserve dignity, restores faith in the system, and often leads to a 3x return on investment (United Way of CT). Moreover, the frequent mention of a lack of financial mobility/opportunity (32 times) and insufficient government assistance (22 times). In about 330 minutes of interviews, our interviewees mentioned every 15 minutes that they felt unappreciated or just plainly didn’t receive the help they needed from the government. This underscores a reality where individuals feel trapped and unsupported by the very institutions meant to serve them. And this is not merely a belief, this is their reality; with many of the interviewees being long-time CT residents and members of the workforce. A Child Tax Credit not only gives the help that so many families need, it tells them that they are important to the state they have worked their whole lives for.

Perspectives on the Child Tax Credit

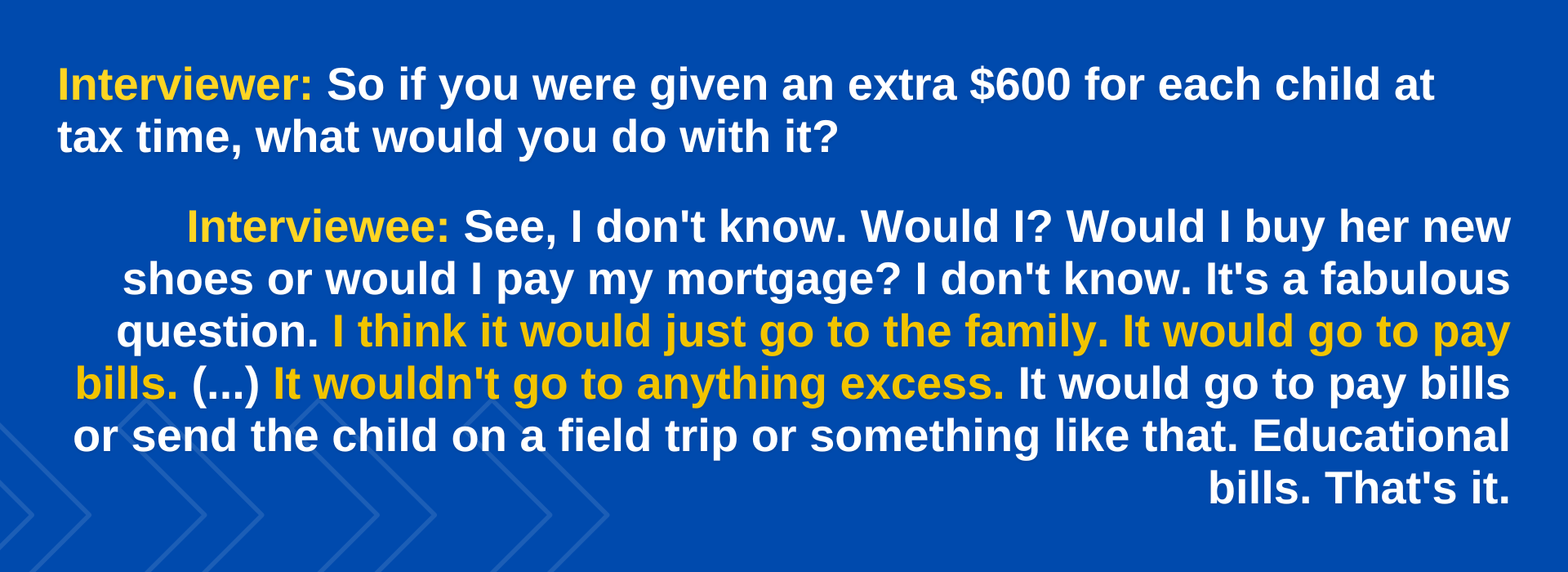

When families were asked if they would be in support of CTC, every single one answered yes saying they would spend them on bare necessities like clothing and food. The unanimous support for the Child Tax Credit (CTC) among families underscores the acute need for financial assistance to cover basic necessities. From clothing to food, these funds are viewed as essential resources to alleviate the strain of meeting day-to-day needs. This perspective reflects a sobering reality: many families are living on the edge, where even modest additional income can make a significant difference in their quality of life. For these families, the CTC represents more than just a financial boost; it’s a lifeline that enables them to secure essentials and navigate the challenges of economic insecurity.

Furthermore, their endorsement of the CTC emphasizes the importance of targeted social policies that directly address the needs of vulnerable populations. It underscores the critical role of government support in providing stability and relief for families facing financial hardship, reaffirming the necessity of ongoing efforts to strengthen social safety nets and promote economic resilience for all.